After a lot of house hunting, you’ve finally found the home of your dreams. A house with the right amount of rooms and a beautiful front yard so, what do you do next? How do you turn yourself into a homeowner from being a potential buyer? It’s simple, you apply for a mortgage to finance the purchase of your new home. As simple as it sounds there’s a lot that goes into applying for a mortgage and one of them is the mortgage underwriting process. If you’re a potential buyer, here’s a Step By Step Detail On Mortgage Underwriting Process.

What is Underwriting?

Underwriting is a critical step in the mortgage approval process where a qualified individual, known as an underwriter, assesses your financial information and determines whether you meet the lender’s requirements for a loan. This process involves a comprehensive review of your creditworthiness, income stability, debt obligations, and the property’s value. The underwriter’s role is to minimize the lender’s risk and ensure that you can repay the loan.

What Is Mortgage Underwriting Process?

An underwriting process merely determines whether a buyer is able to pay back the loan to the lender. It is a process due to the lender, assessing the risk of lending money. The lender here will assess and verify your income, debts, assets, etc. towards the decisive approval for your loan.

What Goes Into Mortgage Underwriting

A mortgage underwriter’s responsibility is to assess the overall risk of the potential buyer, and whether he/she would be able to repay the mortgage. The underwriter evaluates the factors which help the lender comprehend a buyer’s financial condition that including –

- Buyer’s credit score

- Buyer’s credit report

- Property intended to be bought by the buyer

Additionally, the underwriter also aids the lender in determining if the buyer may or may not see a forthcoming loan approval. The motive of this process is to ensure the buyer doesn’t end up closing a mortgage that they can’t afford. An underwriter further will investigate the buyer’s credit history, order an appraisal, verify the income and employment, analyze the Debt-To-Income Ratio, and lastly, verify your payments and savings.

Here’s what an underwriter does:

A mortgage underwriter is a crucial player in the loan approval process. They are responsible for assessing the risk associated with lending to a borrower and determining if the loan meets the lender’s guidelines. Here are some key responsibilities of a mortgage underwriter:

1. Review Your Credit History: This includes a thorough examination of your credit report, credit score, and payment history.

2. Analyze Your Finances: Lenders typically adhere to federal financing guidelines. For example, Fannie Mae guidelines require borrowers to have a maximum loan-to-value (LTV) ratio of 97 percent, a credit score of 640 or higher, and a maximum debt-to-income (DTI) ratio of 36 percent. The lender might also incorporate its own criteria. Additionally, they’ll consider specific aspects of your financial situation. If it’s an income-producing property, they might assess whether you plan to occupy the property alongside tenants and take into account your financial reserves, such as investments, assets, and savings.

3. Conduct a Property Appraisal: The approval of your loan is influenced, in part, by the relationship between the amount you’re borrowing and the value of the home you’re purchasing (used as collateral). As a result, the underwriter will request a property appraisal to ensure that the asking price aligns with recent sales of comparable homes in your area.

4. Render the Approval Decision: Once all the necessary reports and paperwork are gathered, the underwriter makes the critical decision to approve or deny your application.

Common Factors That Can Impact Mortgage Underwriting

Mortgage underwriting is a complex process that takes into account various factors to assess your eligibility for a loan. Let’s explore some of the common factors that can impact mortgage underwriting.

- Credit Score: Your credit score plays a significant role in mortgage underwriting. Lenders use this three-digit number to evaluate your creditworthiness and predict your ability to repay the loan. A higher credit score indicates a lower risk for the lender, making it easier for you to secure a favorable loan.

- Income: Underwriters carefully evaluate your income to determine if you have the financial capacity to make regular mortgage payments. They will assess your employment history, stability, and the consistency of your income. Generally, a higher income level makes you a more attractive borrower.

- Debt-to-Income Ratio: Your debt-to-income (DTI) ratio is another crucial factor in mortgage underwriting. It measures the proportion of your monthly debt payments to your monthly income. Lenders prefer a lower DTI ratio, as it indicates that you have enough disposable income to comfortably handle mortgage payments.

- Employment History: Underwriters consider your employment history to gauge the stability of your income. They typically look for a steady employment track record, preferably with the same employer or within the same industry. Frequent job changes or gaps in employment can raise concerns for lenders.

- Property Value: When underwriting a mortgage, the value of the property you’re purchasing or refinancing is also assessed. Lenders want to ensure that the property’s appraised value aligns with the loan amount. A lower loan-to-value ratio (LTV) is generally preferred, as it reduces the lender’s risk.

Understanding these common factors can help you prepare better for the mortgage underwriting process.

What Information Do Underwriters Look at?

Mortgage underwriters analyze a range of documents and information to assess your eligibility for a loan. Here are some of the key items they review:

- Credit Report: Underwriters obtain your credit report from the three major credit bureaus – Experian, Equifax, and TransUnion. They scrutinize your credit history, including your payment history, outstanding debts, and credit utilization. A clean credit report with a history of timely payments enhances your chances of approval.

- Income Documentation: Underwriters review your income documentation, such as pay stubs, tax returns, and W-2 forms. They verify the stability of your income source and calculate your debt-to-income ratio. Self-employed individuals may need to provide additional documentation, such as profit and loss statements or business tax returns.

- Bank Statements: Underwriters analyze your bank statements to assess your financial health and verify your assets. They look for consistent deposits, large cash transactions, and any red flags that could indicate undisclosed debts or financial instability.

- Employment Verification: Underwriters verify your employment history and income by contacting your employer directly. They may request additional documentation, such as employment verification letters or recent pay stubs, to confirm your income details.

- Appraisal Report: Underwriters review the appraisal report to ensure the property’s value aligns with the loan amount. They assess the property’s condition and location to determine its marketability and potential risks.

By understanding the information underwriters evaluate, you can gather the necessary documents and ensure that your financial records are in order. Now, let’s explore the step-by-step process of mortgage underwriting.

Types of Underwriting Categories

There are three main types of underwriting process. Those are: loans, insurance, and securities.

Loan Underwriting

All loans, in some capacity, undergo the process of underwriting. This involves the evaluation of an applicant’s credit history, financial records, collateral value, and other factors that vary based on the loan’s size and purpose. The appraisal duration can range from a few minutes to several weeks, depending on whether human intervention is necessary.

The most common form of loan underwriting that involves human underwriters is for mortgages. This is the type of underwriting that most individuals encounter. The underwriter assesses an individual’s income, liabilities (debt), savings, credit history, credit score, and more, considering their unique financial circumstances. Mortgage underwriting typically has a “turn time” of a week or less.

Refinancing often takes longer, as buyers facing deadlines receive preferential treatment. The loan applications can be approved, denied, or suspended. The most receive “approval with conditions,” requiring clarification or additional documentation.

Insurance Underwriting

In insurance underwriting, the focus is on the potential policyholder – the individual seeking health or life insurance. The medical underwriting for health insurance was used to determine pricing and coverage decisions. These are based on health status, often considering pre-existing conditions. However, since 2014, under the Affordable Care Act, insurers are no longer allowed to deny coverage or impose limitations based on pre-existing conditions.

Life insurance underwriting aims to evaluate the risk of insuring a potential policyholder based on factors such as age, health, lifestyle, occupation, family medical history, hobbies, and other criteria determined by the underwriter. The outcome of life insurance underwriting can lead to approval, along with various coverage options, prices, exclusions, and conditions, or outright rejection.

Securities Underwriting

Securities underwriting, which evaluates the risk and appropriate pricing of specific securities. That are related to Initial Public Offerings (IPOs), is typically conducted on behalf of a potential investor, often an investment bank. Following the underwriting process, the investment bank may purchase (underwrite) securities issued by the company attempting the IPO and then sell those securities in the market.

Underwriting ensures that the company’s IPO will raise the necessary capital and provides the underwriters with a premium or profit for their services. Investors benefit from the vetting process that underwriting provides, enabling informed investment decisions.

This type of underwriting can encompass individual stocks and debt securities, including government, corporate, or municipal bonds. Underwriters or their employers purchase these securities to resell them for a profit, either to investors or dealers (who sell them to other buyers). When multiple underwriters is involved, it is referred to as an underwriting syndicate.

What Is Automated Underwriting Vs Manual Underwriting

A mortgage underwriter has two options to assess the loan application. The first is to do it manually and the other through software. The one with software is known as automated underwriting. An automated underwriting process is much easier and faster than the manual one as a computer evaluates it. Although, it has some limitations that are non-negotiable like inconsistent income, poor credit score, etc. That may be a deal-breaker for borrowers. Hence, in such circumstances, manual underwriting is an easy option. Furthermore, in some situations, lenders combine automated and manual underwriting to avoid the complications of the loan application.

Mortgage Underwriting Process Steps

As explained above in brief, an underwriter evaluates your finances and forwards them to the lender. Although, there are more aspects that need to be analyzed while proceeding with the underwriting process. Some of the aspects are given below.

1. Income

While assessing a buyer’s income the underwriter requires a set of documents as proof to determine if he/she can cover the monthly mortgage payments. As a buyer, you’ll need to submit documents like –

- W-2 (of last 2 years)

- Bank Statements (2 most recent ones)

- Pay stubs (2 most recent ones)

Furthermore, if the buyer is self-employed or has a share in a business. There are some additional documents that need to be submitted. Such as –

- Profit And Loss Sheets

- Balance Sheets

- Personal And Business Tax Returns

- K-1s

Adding to the above, the underwriter will verify if the buyer’s income is as mentioned in the payslips (or any other format where the income details are provided). Also, the underwriter will verify your employment status with the employer as well.

2. Assets

Your assets help you qualify for a mortgage. As they can sold for hard cash if you fail to satisfy the outstanding loan amount. An underwriter will go through your savings accounts, stocks, and property if any. As the closing amount ranges from anywhere from 3%-6% lenders use assets to make sure the buyer makes monthly payments post-paying closing costs.

3. Credit

It is one of the most important aspects of mortgage approval, is assessing your credit score. An underwriter will evaluate your credit score to understand how well you have managed to repay your past loans. Assessing your credit score helps the underwriter to predict your capacity to repay the loan.

4. Collateral

The underwriter needs to understand the worth of the house you’re interested in buying. The motive for seeing the collateral risk is to avoid putting the buyer’s money in a house that is not worth it. Hence, as a part of the closing process, the lender will order an appraisal.

Potential Underwriting Consequences

There can be only three possible consequences of the underwriter’s evaluation as given below.

1. Conditional / Contingent Approval

You can submit documents to satisfy the underwriter’s questions. Although, you’ll be clear to close while the documents go through the assessment. One of the most common requests includes verification/proving large amounts of deposit in the buyer’s bank. In such situations, a gift /donation letter from the donor is vital to prove it’s not a loan.

2. Suspension

This means there are significant questions in your file for which a loan officer will work with you closely to resolve the underwriter’s questions.

3. Denial

If the buyers got the loan pre-approved and review of their finances thoroughly, their loan will still be ultimately declined.

How Long Does Underwriting Take To Complete?

The underwriting process takes up to 5-8 days. Although, there are dependencies like your financial condition, loan type, missing paperwork, etc. that may prolong the whole process. Additionally, a point to remember, underwriting is a mere part of the process. A complete closing can take up to 40-50 days in total.

Tips for Smooth Mortgage Underwriting Process

1. Organize Your Documents

The key to a streamlined mortgage underwriting process is to have all your financial documents ready before applying for a loan. Keep the following document ready when you apply:

- Employment details from the past two years (for self-employed individuals, include business records and tax returns)

- W-2s from the last two years

- Pay stubs covering 30 to 60 days before application

- Comprehensive account information, including checking, savings, CDs, money market accounts, investment accounts, and retirement accounts

- Additional income details, such as alimony, child support, annuities, bonuses, commissions, dividends, interest, overtime payments, pensions, or Social Security payments

- A gift letter if you’ve received funds from friends or relatives for your down payment

2. Enhance Your Credit Profile

A lower credit score can make mortgage approval challenging and result in a higher interest rate. Improve your creditworthiness by taking the following steps:

- Pay down existing debts

- Avoid applying for new loans during this period

- Aim for a favorable debt-to-income (DTI) ratio (ideally 36% or less)

- Review your credit report for errors and dispute inaccuracies

3. Consider a Larger Down Payment

The underwriter also evaluates your loan-to-value (LTV) ratio, which compares your loan principal to the property’s value. A higher LTV ratio puts the lender at more risk if you default on the mortgage. You can improve this ratio by making a substantial down payment upfront. Borrowing less through a larger down payment increases your chances of qualification. Don’t hesitate to explore down payment assistance programs or seek support from family and friends.

By following these steps, you’ll pave the way for a smoother mortgage underwriting process. Also, well-prepared and maximizing your chances of loan approval.

Takeaways

A pro tip to speed up the process is to keep the documents in place, maintain a good credit score and always put a larger down payment. This way it’ll make the mortgage underwriting process a smooth sail. Furthermore, if you are in a hurry to move out and don’t have time for a traditional home-selling process then sell your house to Elite Properties. We buy houses as-is which means no hassles of legal documentation. We close a deal in less than 7 days and offer you hard cash. Call us today at 718-977-5462 and sell your house fast for cash.

What Are the Steps in the Mortgage Underwriting Process

Mortgage underwriting involves several stages that culminate in the lender’s decision to approve or deny your loan application. These steps are

- The process begins with completing a loan application and submitting it to the lender.

- Once your application is received, the underwriter performs an initial review to ensure all necessary documents and information are included.

- Underwriters analyze your credit report, income documentation, and other financial records to assess your creditworthiness.

- Underwriters review the appraisal report to ensure the property’s value supports the loan amount.

- Underwriters may issue a list of conditions or additional documentation required for loan approval.

- Once all conditions are satisfied, the underwriter grants final approval for the loan.

What are the factors that impact the duration of mortgage underwriting?

Several factors can impact the duration of mortgage underwriting, those are

- Application Accuracy

- Lender’s Workload

- Complexity of the Loan

- Third-Party Involvement

How Long Does Mortgage Underwriting Take?

On average, the underwriting process takes approximately 30 to 45 days from the time of application submission. However, it’s important to note that this timeframe is just an estimate, and the actual duration may differ.

FAQ

What Are the Steps in the Mortgage Underwriting Process

Mortgage underwriting involves several stages that culminate in the lender’s decision to approve or deny your loan application. These steps are

- The process begins with completing a loan application and submitting it to the lender.

- Once your application is received, the underwriter performs an initial review to ensure all necessary documents and information are included.

- Underwriters analyze your credit report, income documentation, and other financial records to assess your creditworthiness.

- Underwriters review the appraisal report to ensure the property’s value supports the loan amount.

- Underwriters may issue a list of conditions or additional documentation required for loan approval.

- Once all conditions are satisfied, the underwriter grants final approval for the loan.

What are the factors that impact the duration of mortgage underwriting?

Several factors can impact the duration of mortgage underwriting, those are

- Application Accuracy

- Lender’s Workload

- Complexity of the Loan

- Third-Party Involvement

How Long Does Mortgage Underwriting Take?

On average, the underwriting process takes approximately 30 to 45 days from the time of application submission. However, it’s important to note that this timeframe is just an estimate, and the actual duration may differ.

As a seller, you simply can’t deny the fact that there’ll always be a lot of paperwork involved while selling your house. Whether you pick a real estate agent for a home sale or you do it yourself, there’s no running away from the verification and paperwork. Home selling is a big transaction and if you need to know what goes into a home selling process then read this blog till the end, ‘Selling house by Owner? Check The Paperwork You Need’.

Where To Find The Right Paperwork?

Starting off, different states have different laws and you’ll have to line up all the necessary documents according to your state. It is extremely vital to do your research and gather all the information before proceeding with showings. Now the question is how and where do you find the appropriate documents to sell your house by owner?

A real estate attorney can help you provide all the information and legal documents that you need while selling your house. Keep in mind hiring an attorney will require fees, so make decisions on your suitability. Additionally, there are also state and county government websites that help you find relevant information.

Documents Needed For A Home Sale

Given below is a list of documents that you’ll require before proceeding with the home sale with the process. (Note: the documents mentioned below may differ depending on the states you reside in)

-

Property Survey

A survey document determines the boundaries of the specific land or property based on the legal documents filed on it in the past. The document also includes details about fences, driveways, etc. if any.

-

Receipts And Warranties

The document helps in documenting information on any new appliances or improvements done to your house.

-

Plans And Permits

This document ensures that you have made changes or upgrades in your house with due permissions, additionally, it’s proof for the potential buyer to cross-verify.

To get this document you’ll have to visit the municipality, get the permit pulled post which you’ll have to get an inspection done, do necessary repairs, and again get the house inspected again. The certificate signifies that your house is safe to reside in and is compliant with all the building codes.

-

Loan Documents

The document usually comprises your first mortgage, second mortgage (if any), and any home equity lines of credit (if any).

-

Latest Utility Bills

The document showcases the monthly amount spent on the household such as electricity, gas, water, etc.

-

Latest Property Tax Bill

The bill gives an idea to buyers of how much tax they’ll pay post purchasing the home.

-

Title

This document shows that you own legal/equitable interest in the property.

-

Homeowners Association Covenants and Agreements

This document signifies a detailed set of rules established by the body that governs the neighborhood. The rules usually contain information about pets, noise level maintenance, etc.

-

Floor Plan or Blueprints, If Available

Having a plan or a blueprint of your house makes the buyer understand in-depth about the property. Make sure you have two sets of all the documents, furthermore, make sure to add anything that pertains to the ownership of your house.

Selling House by Owner, Here’s How You Do It

If you’re stuck with limited funds, selling a house to an owner is the ideal way out. To know how it’s done follow the process below –

-

Assess Your Property’s Value

Always assess the value of your property before listing it. There are certain setbacks while you list your house like over or underpricing. What do you do in a situation where you are aware of the drawbacks? First off, check the estimated value of your house from home value sites available on the internet.

By only paying a small amount for an FSBO home evaluation you’ll have a licensed professional who’ll do an in-depth evaluation of your home. In 5-7 business days the person will visit your house and you’ll have a detailed report in your hand.

-

Get Your Home Sale Ready

It is an unsaid rule to keep your home in its best shape before putting it on the market. You might want to showcase your home’s full potential by rearranging furniture, decluttering waste, and giving your walls a fresh coat of paint.

-

Promote Your Home’s Sale

As old-school as it may sound, putting a sign in your yard saying ‘for sale’ makes a lot of difference in the sales. People in the neighborhood will take note of the sign and spread the word. Furthermore, list your house on famous FSBO (For Sale By Owner) listing sites and MLS (Multiple Listing Service) and take that extra step to generate more traffic to your house.

-

Negotiate The Sale

A buyer will always offer a price that’s below the asking price or ask you to pay the closing costs, here’s when you have to negotiate. At this stage, you’ll need documentation, within days of accepting the buyer’s offer it is mandatory to have a copy of their mortgage approval. Post this the buyer will submit a written offer that is mutually acceptable. It is only now that you must draw up a contract that includes closing concessions, final price, closing date, location, and a list of contingencies.

The contingencies are put in the contract by keeping in mind the buyer’s security and allowing them to back out if things fall out of place.

-

Close On the Sale

A closing may either take place at the real estate attorney’s office or the title company depending on the state laws. Make sure everyone is on the same page and the communication is free of any loopholes as the date of closing is the final stride to complete the sale.

-

Disclosure Statement

What is a disclosure statement? It is a document required by most states that outlines defects of the property. It may include mold, flooding, lead paint, radon, structural problems, etc. A disclosure statement protects the seller from any post-sale claims made by the buyer of which they didn’t know initially. Fill out this Disclosure Form before selling the property.

Things That Must Be Included in a Real Estate Contract?

Here’s a list of things that you must touchdown while drafting a real estate contract –

- Property And Its Characteristics

- Identity Of the Parties Involved

- List Of Fixtures/Personal Property

- Purchase Price

- Earnest Money Amount and Financing Terms

- Target Closing Date

- Contingencies

- Proration

- Title

- Closing Cost

- Notice Or Default Legalese

- Miscellaneous Provisions

Conclusion

If you’re a first-time seller and trying to sell your house on your own, we hope the blog might help you in the process. Furthermore, if you wish to sell properties online you can contact Elite Properties, we buy houses New York and if you want to know more about the process of selling house by owner, contact us today at 718-977-5462.

The facade of real estate has changed with time and new-age processes like virtual tours, virtual staging, advertising online, etc. , are pulling the limelight. With the moving age of the internet selling and buying is as easy as a click. The dynamics of business are constantly evolving whether it’s real estate or groceries. People prefer convenient alternatives rather than the traditional home selling process. Nowadays, people are attracted to iBuying, don’t know what is it? Scroll through our blog, ‘Is iBuying Worth The Hype? What is an iBuyer?’ to know more about the topic.

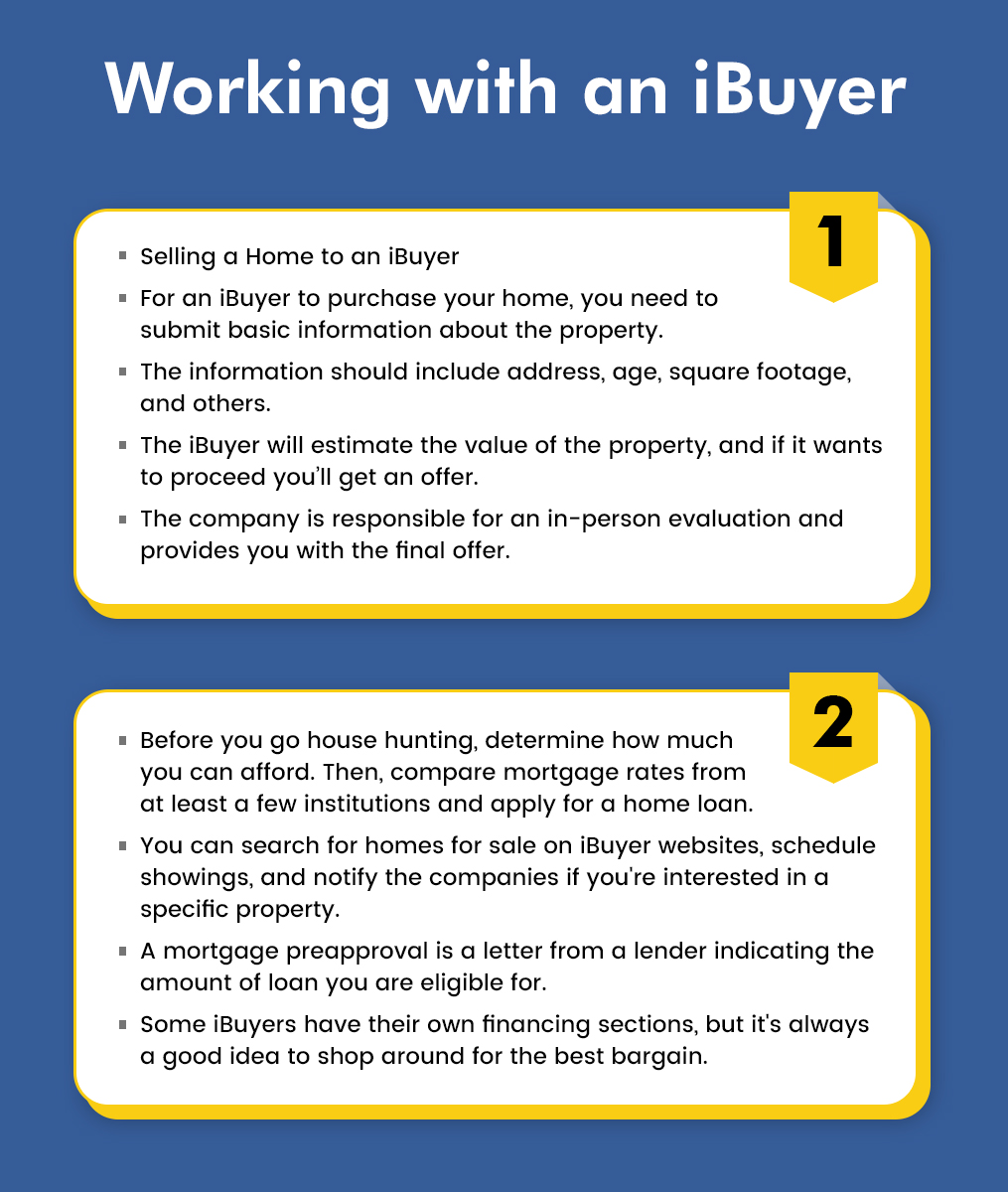

What Is An iBuyer?

To put it in simple words, an iBuyer is a company with ample finances that makes an offer on your behalf based on algorithms. The term “iBuyer” is a fusion of words where I denote ‘instant’ combined with the word ‘buyer’. The company makes all the trades and makes the whole process convenient for both buyers and sellers. iBuyers try to sell your house with a profit margin and give you cash in return once sold.

iBuyers buy your house as-is which means selling your house without spending a ton of money. It enables a buyer to avoid the extra upfront costs that incur while closing. Additionally, it avoids the need for real estate agents or brokers.

How Does An iBuying Model Work?

As given above iBuyers use algorithms to determine the ideal price of a home, which are based on comps (comparables). The iBuyers provide instant offers to sellers in as few as 24 hours once you fill out the requisites in the form. A potential seller will have to go to the iBuying website and fill out a form, post which they receive an offer. For instance, if the seller accepts the offer then the sale is likely to close in just a few weeks.

How do iBuyers make profits?

iBuyers usually buy a property with a discount as-is. They add value to the property by making minor improvements to optimize the selling price post which they list on MLS. Additionally, iBuyers provide an in-house financing service to customers which helps in earning good profits. A service charge typically ranges from 5% (can be higher or lower, relies on the tenure of selling your house)

Pros And Cons Of Selling Your Home To An iBuyer

iBuying is a great way to close deals fast, although it comes with a set of pros and cons. Some of them are given below.

Pros of iBuying

- Capable of fast closings (as less as a couple of weeks)

- Avoid the hassles of legal verification, inspection, or appraisals

- Does not require walkthroughs

- Avoid paying the upfronts costs while closing deals

Cons of iBuying

- May require some amount as a listing fee, which is usually higher than a real estate commission

- Currently, only a few iBuying companies are active and providing services

- Less selling prices, usually below the fair market value

- In most iBuying models the house may have to satisfy the ideal house criteria

Is iBuying Really Worth It?

Whatever method you use to sell your house whether it’s a traditional home sale or iBuying, will have some advantages and disadvantages. It is all about what suits you best. Although, if you choose to sell through an iBuyer, make sure to do your due diligence. Besides, it is equally important to go through all the fine print and policies including the other costs and fees if any.

Conclusion

If you are someone who wants to sell your house fast and doesn’t have enough time to wait? You can get in touch with Elite Properties. We buy houses for cash online in New York and offer you enticing deals over your as-is property. Furthermore, if you wish to learn more about a house sale then call us at 718-977-5462, we’ll be happy to help.

When it comes to a home selling process in real estate, selling psychology is always a part of it. When you sell your house there’s always an underlining message you put out for your buyers. You may not be aware of it but you’ve been sending these messages to buyers secretly. In these cases, you might want to send the right message to potential buyers. It is essential to understand the demography of buyers and your locality. For eg: If there are grad students residing in your neighborhood or there might be a retired couple. When home selling psychology comes into play, you have to picture who your ideal buyer is and think accordingly from a buyer’s perspective.

Clutter Can Be A Strong ‘NO’ For Buyers

For a buyer, it is important to feel homely while picturing themselves in the house they’re visiting. When you have your personal belongings lying in the house while walkthrough, sellers may feel a bit intrusive. No buyer should feel as they are invading your personal space rather should feel homely and imagine themselves residing there.

What’s The Solution?

Cleaning up personal items such as trophies, family portraits, collages, etc. can help avoid such awkward situations.

Take Time In Preparing Your Home

Buyers will never make significant changes in the house unless they’re a real estate investor. If a buyer has infants or toddlers in a family they’d not buy a house with a pool or lavish landscapes. Besides, even staging your house excessively will have certain drawbacks. In order to keep your home tidy, you don’t necessarily need to stage it. A well-planned staging with minimal neutral upgrades can sell your house fast for cash. Eventually, it is vital to understand the buyer’s demography and make upgrades accordingly.

What’s The Solution?

As it might be difficult for you to understand initially who your buyers are? You can always switch to keeping the tone of your house neutral. Having a neutral room can allow buyers to put ideas into perspective. However, you can do basic upgrades like plumbing and fixing the roofs, etc., and avoid extra decor to make your house look beautiful.

It Is Important To Have A Purpose

Defining the purpose of each room can sell your house fast. Most people have a room for multiple purposes. For eg: A storeroom, which is also your gym or office space that has a play area. If this is the condition of your rooms as well then you might want to start defining the purpose of each room. Setting a room that is multifunctional can be practical for your family. Although, as a potential buyer it can still be a little confusing for them to understand the purpose of the room/s.

What’s The Solution?

If you have a total of 3 rooms excluding the kitchen and living area make sure the other three rooms are plain and neutral. Avoid creating chaos by having a multipurpose or multifunctional room while selling your home. Let the buyers have the advantage to think about how the rooms can serve their purpose.

Sell Your House With Elite Properties

A traditional home for sale method will require money, time, and energy. You can contact Elite Properties they are cash buying company that provides cash for homes New York. Selling house to a cash buyer (selling psychology) is much feasible as they don’t charge you any upfront costs. You can sell your house within 3 days in any condition and we will pay your closing cost. Call us today for an offer at 718-977-5462.

Do you wish to sell properties online but don’t know whom to approach? Well, we are here to suggest and help you pick the right person. Many homeowners contact real estate brokers to sell their homes so that they can make more money. You can also contact Real Estate Investors to sell your house. But, it is advisable to consider both before choosing one to determine which one suits you the most.

You might think what is the difference between both of them anyway? The difference is negligible as they both generate revenue from the same field. Scroll down to know the difference between a real estate agent and a real estate investor.

License Plays an Important Role

To make valid transactions it is important for a real estate agent to have a license. An agent requires a license of his/her particular state of service. An agent should have a license to act as a representative for other people to buy or sell homes. On the other hand, an investor does not require a license to run the business.

Commission Has Different Aspects

The commission involves agents and investors, while the methods of extraction are different.

What is Real Estate Agent?

Real estate agents earn a commission on every sale carried out by them. The amount can be anywhere from 1-5% of the total share inclusive of the other costs. Agents rely on the sale price of a property to determine how much commission they receive. The higher the price, the higher the commission.

What are Real Estate Investors?

Maintaining The Integrity of the Brand Has Diverse Ways

Real estate agents make sure to market their brand name to attract clients. Networking using websites and business cards can help Agents to expand their network. Real estate investors on the other hand do not spend a lot on marketing. They use signboards with ‘we buy ugly house’ or ‘we buy house for cash’ written on them. These signs are placed in cities or nearby yards, which can be easily spotted from a distance. Retaining the integrity of the brand may have different modes, but the motto stays the same.

Involvement of the Brokers

Real estate agents have to work under brokers. Agents work for brokers after completing their training and receiving a state-issued license. A real estate investor does not have the need to work under a licensed broker isn’t mandatory.

How Elite Properties Is Better Than Any Other Agent

Agents: Real estate agents sell home with the help of MLS also known as Multiple Listing Service

Elite Properties (Investor): We buy houses individually without any listings

Agents: You’ll have to pay closing as well as additional costs to cover a sale.

Elite Properties (Investor): We cover everything inclusive of closing costs and legal fees to make your home sale process easy

Agents: A traditional home sale through an agent will take approximately 30-60 days to close a deal

Elite Properties (Investor): We close a deal in as less as 7 days

Conclusion

Picking the right person to sell your house is vital. One has to research their options before proceeding with a home sale. Elite Properties is a cash buying company, we sell your house in 3 days in any condition and at any location. Furthermore, we will also pay your legal fees and closing costs. Call us at 718-977-5462 or visit our website https://www.elitepropertiesny.com/ to know more about the home selling process.

There is always a debate amongst people about what is better. Buying a House Cash vs Mortgage? In this blog, we will try to clear the picture and try to help you in the home selling process. A lot of finance experts say buying a house in cash can avoid drowning in debt. Although, the other half believes in getting a mortgage and repaying it over the 15/30-year mortgage. Every method of purchasing an asset has its pros and cons. We will share an overview of each method and how it varies in each situation.

Why Must One Buy House in Cash?

In simple terms buying your home in cash allows you to avoid foreclosures and you are free of debt. You have complete ownership of your assets as you buy the property in full cash. Although every scenario has its pros and cons, scroll down below to know more.

Pros Of Buying a House in Cash

-

Free Monthly Cash Flow

One of the big reasons to buy a house in cash is free cash flow. If you buy a house in cash you aren’t entitled to pay monthly mortgage installments. It allows your income source in multiple bifurcations as per your convenience and needs. Although, you’d still be paying the homeowners association fees, property taxes and maintenance costs, homeowners insurance, etc. You will pay these extra costs even if you don’t get your house on mortgage. When you buy a house on a mortgage, you pay a big chunk to the lender whereas in this case, you avoid it entirely.

-

Save A Lot on the Interest

If you purchase a house in cash, you can save a lot on the interest of the mortgage. When you take out a mortgage, the interest rates are bound to escalate over the tenure. Example: A mortgage of $170,000 having a 4.375% interest rate costs you around $135,000 as interest expense for 30 years. Furthermore, mortgage debts are one of the cheapest in the USA if calculated on the APR (Annual Percentage Rate) basis. So, buying your home in cash might save a big chunk on the repayment.

-

You Are a Preferred Prospect

Sellers always prefer cash buyers as the deal closes faster. When a seller sells the property to a cash buyer, it only requires the buyer’s due diligence and mutual closing date. Whereas, when a buyer applies for a mortgage, he/she has to work on a lot of things. Things like the verification process, legal documentation, the underwriting process, etc. The real estate market is big, but sellers usually pick cash offers as they are enticing and close faster. Also, a cash offer allows negotiation in closing costs as you trade in hard cash. If you are a cash buyer, you’ll be the preferred prospect instead of the one with a mortgage.

-

Faster Closings and Lower Closing Costs

When you buy a house in cash, you avoid paying the associated loan fees. Also, costs like the originating fee, mortgage insurance premium, credit card report fee, etc. A cash offer may help you get away with legal processes and verification. Remember, an all-cash offer is less than the traditional bidding price. Getting paid in hard cash eventually is better than the orthodox mortgage bid, which is time-consuming. Additionally, as stated above, you close a deal faster with flexible closing costs.

Cons Of Buying a House in Cash

-

Tying a Lot of Money into One Asset

If your property is worth $150,000 and you are a cash buyer, it can be quite risky. If you invest a large amount of your savings in one asset, you are tying up a lot of money. Such transactions do not show a positive outcome on your credit score.

-

Low Liquidity

The real estate market or a house is an illiquid asset, which means it is difficult to sell it fast. Selling a home is time-consuming and a daunting task. Assets like bonds and stocks which have high liquidity are easy and quick to resell whereas a house is not. Therefore, putting a lump sum amount in one asset is never ideal as it slumps access to the liquid assets.

-

Missing Out on Tax Benefits

The itemized taxes may help in putting the money back in your kitty. You can deduct a lot of amounts on mortgage rates through itemized taxes. Itemized tax deductions levy on multiple assets; it is advisable to check the taxes before purchasing. If you are using cash as your primary payment source then you are definitely losing some good tax benefits.

-

You Are Left with No Savings

Buying a house in cash blocks your savings, and you have nothing, which means no emergency funds. It is always advisable to keep petty cash handy during an unexpected crisis.

Why You Must Consider Getting a Mortgage?

Buying a house on a mortgage allows you to maintain your savings and caters to the funding. Many people do not have enough savings to buy a house in cash. Prospects get a mortgage and keep building the equity over the tenure of repayment.

Pros Of Buying a House on a Mortgage.

-

Flexibility Savings

When you get a mortgage, you have the flexibility to put your savings into other investments, which promise good returns. You can pick from innumerable liquid investments and grow your wealth and manage your monthly payments as well. Buying a house on a mortgage is always a better option as you have more flexibility to manage the money.

-

Low Mortgage Rates

Comprehending the pandemic and the current state of the market, it’s a better option to opt for a mortgage. The mortgage rates are low, and the inventory has houses sitting for potential buyers. Hence the above makes it an ideal situation for purchasing a home.

-

Improve Your Credit Score

If your credit report shows timely repayments, you will ultimately have a good credit score. Unlike buying a house with cash, it is essential to show the diversity of debts for a better credit profile. Credit reporting agencies prefer timely repayments of debts including home loans. It improvises the borrower’s profile allowing them to get a faster mortgage and boosting their credit score.

-

Advantages Of the Tax Deduction

Mortgage debts are tax-deductible, which means more benefits for the person getting a mortgage. Married couples planning to buy a home can write off interest taxes up to $750,000 if filing together. If you are filing separately, you can write off tax interest up to $375,000. Post the tax reform in the year 2018 write-offs were not as profitable. Although it still is beneficial for homeowners with outstanding mortgages.

Cons Of Buying a House on Mortgage.

-

The Intricate Mortgage Process

It’s no hidden truth that getting a mortgage can be a really daunting and tiring process. You have to keep track of all financial documents inclusive of your IDs, which can be frustrating at times. Lenders will ask you for every detail and if you miss even a single document, you won’t qualify for the loan.

-

Paying Mortgage Insurance Premiums

When you pay less than 20% on the property, having a mortgage insurance premium will be mandatory. A mortgage insurance premium is an addition to your monthly mortgage payments. Insurance is an added cost to secure the lenders in events if you miss out on paying the installments.

-

Drawback Of Additional Costs

When a mortgage has lenders involved, it always comes with extra costs. The buyers are liable to pay lender fees, closing costs, mortgage origination fees, and appraisal fees. These additional fees can add to the existing cost and make the purchase even more costly.

-

You Still Don’t Have the Ownership of the Property

When you buy a house on a mortgage, the lender has ownership while you keep making the monthly payments. They are entitled to hold your property until the last installment. If you fail to pay a consecutive number of installments, there is a high risk of losing your home.

Bottom Line

We know buying and selling a home is an overwhelming task. It can be a very confusing, lengthy, and mentally draining process. We tried to cover the pros and cons of buying a house in cash or by getting a mortgage. So, choose wisely keeping in mind your monetary status and plan futuristically.

If you are planning to sell your house fast for cash in NY, get in touch with Elite Properties. It is a ‘We Buy Houses For Cash Company’ which means you can sell your house fast for cash. Give us a call on this number at 718-977-5462 and we’ll help with fast home selling.

COVID-19; A horrifying pandemic crisis that the world is facing right now. As the situation is affecting many sectors around the globe, real estate isn’t left behind. The raging effect of COVID-19 has created a major void in the market. This resulted in a huge downfall with respect to the world market and economy. Let us look deep into the Foreclosure And Short Sales Market.

Many services offered by the real estate market like walkthroughs, rentals, etc. had been hard hit by the virus. As these aren’t the only services that have suffered, other facilities like foreclosure and short sales have also been adversely affected. In this blog, we will tell you How COVID-19 has affected the Foreclosure and Short Sales Market.

The Imprint of Coronavirus on the Foreclosure and Short Sales Market

As everyone is witnessing the catastrophic situation of coronavirus, its effects are also visible with respect to the economy. The loss industries have been facing is immense and would take a while to make up for the loss. Although, the foreclosure market is going through an uptick. According to the research by FTSE (Financial Times Stock Exchange) and REITs (Real Estate Investment Trusts) says there’s an evident index downfall of approximately 7.7 percent (noted on March 9, 2020).

If this goes on for some time, it would be difficult for homeowners to keep up with the monthly mortgage payments. It will later result in increased foreclosure cases, although it is tough to predict the real estate market. As facts state, in some states, the mortgage payments are being held for some time until the pandemic contains.

Coronavirus has Pushed Mortgage Rates Lower

The coronavirus outbreak has made the Federal Reserve take two emergency rate cuts. This apparently brought the bond yields to almost zero. The usual 30-year-fixed-rate-mortgage has dropped to 3.29% (noted on 5 March). As stated in the records, previously the 30-year-fixed-rate-mortgage was lowest in the year 2012 amid the recession when it hit 3.31%. Additionally, the 15-year-fixed-rate-mortgage also fell by 16 basis points to 2.79% according to Freddie Mac.

The main cause of the mortgage rates slump is because of the treasury market which has sunken with a lot of margin in the past months. Furthermore, the uncertainty of mortgage rates shall remain in the ditch for a long period.

Corona on Short Sales

When businesses are close around the globe and many of them can’t go on their jobs. So, homeowners have no choice but to sell their houses for a living. Homeowners with no jobs have the only choice but to sell their houses for the bare minimum profits. This measure is to perform their regular routine and satiate their daily needs. A short sale can cost less than a foreclosure to the lender. This always proves to be the most viable way for lenders to minimize the loss and improve profits. Additionally, a short sale might not damage the credit score of a homeowner.

If you have a hefty amount of mortgage to repay then your only possible option is to fulfill the amount. You can do it by selling your house to a cash-buying company. As there is a rapid increase in short sales it is evident that problems like unresponsive lenders, misplaced documents, erroneous or unrealistic home value assessments, and prolonging processes may make the whole process difficult. In such a chaotic situation, Elite Properties is one such company that will help you sell your home fast for cash on a fair market value. We also buy your house as-is. We won’t ask for any lengthy documentation process, which automatically cuts the hassles of a troublesome sale.

You can call us at 7189775462 or visit us at Elite Properties NY to learn more about the home selling process with us. Where everyone around the world is going through the pandemic crisis we’ll help you be at ease with the home selling or short sale process.

If your house isn’t selling, it can be a big problem and a matter of extreme stress to homeowners. If it has been sitting for a long time in the market, it will ultimately lose its value. Simply tweaking your marketing skills and changing your home selling process can favor you a lot. If you think you’ve tried everything, then think again or scroll down below and go through the 7 Tips On How To Sell An Unsellable House.

Postpone The Home Selling Dates for your Unsellable House

Setting the right time to sell in the market is extremely essential as the price you may achieve certainly relies on it. It is a known fact that real estate is majorly a seller’s market and you’d need to know about the pattern of selling homes. There is a certain time of the year when the sales are highest, spring is the ideal time to sell your house or put it on the market. Whereas, winter is the time when sales are comparatively low. If you’re not up for the seasonal sale pattern then there’s another way where you can wait for the inventory to drop and then put your home on the list.

Try Selling Your House Under The Market Price

Mispricing your home can be the easiest mistake you can make while listing your home, so the ideal way to entice buyers is by selling your property for a lower market value. Buyers or real estate investors are always on a hunt to find houses that are priced for less than their fair market value, this kind of sale is also known as ‘fire sale’ according to the real estate lingo.

This might not be your ideal choice but in this state of utter despair, this might be the most enticing option for you. As investors are constantly looking for such deals, some companies might actually surprise you by buying your property in as-is condition for a fair price. Try selling your house to a ‘we buy house for cash’ company; Elite Properties New York will buy your house in any condition and additionally offer you a no-obligation offer.

Consider Deep Cleaning, Improvements, And Curb Appeal

A clean house will always sell for a huge profit, keeping in mind its functional aspects of it. Fixing serious issues like your electrical and HVAC system will work wonders if they were in a rough condition. Plumbing, windows, and checking for leakages from roofs or sewage pipes are important points to remember. Make sure all the functional aspects of the house are covered before selling. If you’re not able to cover the improvement’s expense then include it as an incentive with the house.

The next important thing to focus on is the curb appeal of your house. If a home isn’t good-looking from the outside it’s never going to sell. You can counter the easy and less pricey things first and then move on to the costly improvements as and where needed. Just cleaning the sidewalks, mowing the lawn, and cleaning the exteriors of your house can make a visible difference.

Up Your Marketing Game

It’s all about the virtual world these days; the easiest way to list your home on the market is by putting it online for people to take a view. Adding to the rest, the results will only show if you market your home right. MLS or Multiple Listing Service can be extremely handy once you choose to put your home online, this particular service enables you to find the right buyers on a wider platform.

Good marketing is equivalent to profitable sales so while listing your home make sure you’re putting out precise information for prospective buyers. Click sharp images of your complete house and also try making a video from the entrance to each room for a better perspective for buyers. A buyer would possibly skip pictures but not a video; make sure the quality of your video is clear, crisp, and shot in bright light.

Documentation Of Property Is Essential

If you’re putting your unsellable house on the market it is important for you to keep complete written information about your property and the changes made or required in the coming future. Keeping updated information about your property will help you in an easier sale and would promise better profits. No matter whether your house is in whatever condition it will always be sold for a fair price if you’ve been transparent with the potential buyer.

Think Through A Short Sale

This might be your last option to reach the final results and achieve a fair price on your property. In most cases statistically quoting; people end up owing more than the property’s worth which is practically impossible to remunerate. There are cases where most of the lenders (in case you have an outstanding mortgage) may or may not agree to a short sale additionally, not every seller will qualify for a short sale. In such circumstances, it is best to opt for a short sale although it is important to do your research before diving in.

Sell Your Home For Cash To Elite Properties

Going through a mortgage, debts, improvements, and on top of it selling an unsellable house can be a lot to bear. In such an unfortunate condition your first option should be selling your home for cash to cash buying companies in New York like us. Selling your home for cash to us might be a boon in an ugly situation. We buy houses as-is which means you are saved from the hassles of making repairs. We close the deal in as less as 3 days which means you can take your money and repay your debts in no time.

guarantee a fair all-cash offer with an additional no-obligation offer where you can terminate the proposal and you won’t have to pay any commission. If the deal is finalized we’ll also pay the closing and associated fees, so what is stopping you? Sell your house for cash to us and we’ll promise you a profitable all-cash sale. Call us at 718-977-5462 or visit us at Elite Properties to sell your house today.

Losing your job is a very tense and stressful situation after which selling your house becomes the only feasible option. The burden of covering insurance and mortgage stands to be the need of the hour. In such circumstances, you wouldn’t want to wait for the traditional home selling process which can take months or even years. If you want to learn about the topic of ‘How do I sell my house fast after a job loss?’ scroll down below to get the insights.

Selling your house to ‘we buy houses for cash’ company will help you in many ways especially when a financial crisis comes into play. Many foreclosures occur due to job loss and unemployment or homeowners’ lack of cash, which becomes a problem while you pay mortgage or insurance. As a fact, foreclosures can lead you to bankruptcy and you won’t be given any loan further as your credit score is affected.

Avoid the Hassles of Clean-Up and Repairs

In such tight constraints, it is almost impossible to give an aesthetic change to your house. Making physical changes or cleaning your house can be time – consuming whereas, staging your home can be extremely costly. Furthermore, it is difficult to find buyers who would buy your house in a traditional way. Here, you can get in touch with ‘we buy house as-is’ companies and they will take care of the rest. There is no need to spend a dime on de-cluttering of your house, staging, or improving the curb appeal, once you get in touch with them.

No Need to Listing Your House on the Market

Listing your home on the market requires a lot of time, the process can last up to many months until you have found a serious buyer. People end up hiring a real estate agent which again is an additional cost while they have a naught budget. An Agent will always end up advising you to stage your home and make it presentable before you list the home on the market. Not forgetting, you will have to pay around 6% commission for the services they provide adding to the rest, closing costs and tax fees are the left-out aspects that round up the deal while closing.

You can also chuck the process of the walkthrough, as it typifies energy, money, and time consumption. It is a long process that doesn’t elude the havoc created by inviting strangers to have a look around your place. Showings additionally can hamper your timeline as well, instead of finding ways to achieve an income source you end up showing your house to strangers who’d hardly care to buy.

Sell Your House Fast For Cash

Lastly, all you can do is sell your house fast for cash and save yourself from the frustration of the home selling process. Selling your house to Elite Properties can save a lot of your time and money altogether in one, how? We are a cash buying company which means we buy your house as-is without any commissions lying in the middle of the road. We propose you a no-obligation offer and buy your house at the current market value which means; only profit and no loss. We also pay the legal fees and closing costs. It is also advised you do some research around the neighborhood and get insights into selling your house.

The most feasible option is to sell your house as-is to us, rest assured we’ll help you in this tough situation. Call us today at 718-977-5462 or visit us at Elite Properties.