Introduction

The home selling process does not necessarily require long commitments or huge levels of stress. Many homeowners dealing with the real estate market in New York City struggle through what amounts to an endless cycle of doubtful conditions and delayed timelines plus hidden expenses. Standard home-selling practices demand lengthy property listings and constant showing activities along with numerous buyer requests that exhaust real estate sellers.

At Elite Properties, a house-buying company, we offer access to a simplified process to sell homes with ease while inheriting total control over your selling timeline. Our team exists to assist homeowners who require urgent house sales or seek an accessible method that eliminates property requirements and open house difficulties.

Our goal is to give homeowners a time-saving and stress-free way to sell their properties which allows them to advance to their future confidently.

Why Selling Your Home Quickly is So Important

If you are wondering “I want to sell my house but how do I do it quickly”. We understand that selling a home quickly is more than just about convenience, it’s often a necessity. Uncertainty about the future can push homeowners to seek urgent solutions. So let’s explore some common situations where time is of the essence:

- Financial Urgency

Life happens. Homeowners face medical crises together with spiraling debts or unplanned financial demands that force them to seek quick solutions for their properties. When dealing with time-sensitive home sales the traditional real estate process often proves unsuitable. A fast home sale creates monetary opportunities by delivering needed financial stability at critical moments. - Job Relocation

An annual total of 35 million Americans relocate for various reasons including job changes. People starting a new job outside of their current city typically lack the time needed to handle home preparation for market listing. Moving forward with your professional transition becomes less stressful when you sell your property quickly through an easy home-selling process. - Avoiding Foreclosure

You face severe mental pressure when dealing with foreclosure as it proves exceptionally complex. Getting into this situation negatively impacts your credit profile so future home buying becomes increasingly difficult. New York residents faced 2,500 foreclosure filing cases during 2023. Quickly selling your home prevents foreclosure so you can protect your future finances and peace of mind. - Saving on Carrying Costs

Owning a home on the market costs you money each month because you have to pay mortgage payments and property taxes along with insurance and basic maintenance bills. Prolonged home ownership creates multiple payments which build up and reduce your financial resources. Elite Properties will give you a swift home sale solution that lets you keep your funds intact when you face ongoing costs.

Why Traditional Methods Aren’t Always Ideal

The standard practices of home selling function appropriately but they don’t suit all potential sellers. Here are a few reasons why:

- Delays in Financing: Bank loans remain crucial for homebuyers yet delays in mortgage financing cause up to 30% of home sales to fall through or stall before completion.

- Costly Repairs and Renovations: Selling your property will require you to spend money on needed upgrades and repairs before attracting potential buyers since these duties can be costly and take plenty of time.

- Uncertain Timelines: In traditional sales transactions you often need to wait multiple weeks or months until someone makes an offer so the closing process remains uncertain.

These roadblocks become daunting for people who want swift house sales. Elite Properties offers a solution that eliminates both the financial burdens and the unpredictability of real estate deals.

What Makes Elite Properties Different

At Elite Properties, we do things differently. We are a reputable house-buying company focused on offering simple solutions for sellers. Here’s how:

- Cash Offers

The cash offers we make to customers eliminate the payment delays and financing requirements that traditional buying methods require. Our process enables you to sell without worrying about financing problems that could ruin the deal with buyers. - Sell As-Is

When you work with Elite Properties your home can be sold without repairs or improvement. You can sell your house in any condition because we don’t require roofing repairs, wall painting, or deep house cleaning. Our solutions handle every detail independently so you remain free to ignore all work. - No Fees or Commissions

Unlike traditional sales, you secure every cent of the cash offer when you sell your house to Elite Properties. - Flexible Timelines

Our service adjusts to your pre-established timeline no matter if you want immediate closing or need time to prepare your moving arrangements. Through the house-buying process, you dictate when each stage of the sale occurs.

How to Sell Your Home with Elite Properties

We’ve designed our process to be as simple and hassle-free as possible. Here’s how it works:

Step 1: Initial Contact

Contact us at 718-557-9261 or explore our website on the internet. The friendly members of our team will walk you through the steps and obtain essential details about your property.

Step 2: Property Evaluation

Our team evaluates two things about your property:

- Its current condition

- Market value

Evaluation happens speedily without requiring expensive appraisals or inspections for your property during this process.

Step 3: Receive a Cash Offer

After evaluating your property we will give you a no-obligation cash offer that matches the property’s fair value. At your own pace, you have the flexibility to determine what solution suits you best.

Step 4: Closing Process

Once you choose our offer, we will manage all necessary documentation and logistical requirements. The sale finalization process happens quickly as we aim to complete it within just a few days.

Step 5: Get Paid

Upon completion of the closing process, we will deliver your payment funds directly without any hold-up period whatsoever.

Why Choose Elite Properties

Selling your home with Elite Properties comes with unmatched benefits:

- Speed: Elite Properties lets you exchange months of waiting for swift home sales without delays.

- Convenience: With Elite Properties you avoid staging while receiving maintenance-free fast cash deals through streamlined sales processes.

- Stress-Free Process: Through us, you eliminate the stress of negotiating prices and inspections and avoid repair maintenance expenses.

- Flexibility: You can make a deal happen with flexibility by setting a personalized timeline as per your requirements.

Where Do We Operate

Elite Properties proudly serves homeowners across all five boroughs of New York:

- Brooklyn: With operations in both Williamsburg and Brownsville we offer town-wide property services.

- Queens: Our team has deep market knowledge across every part of Queens from Astoria to Flushing.

- Bronx: As a real estate firm we also work to help Bronx homeowners complete their sales without stress.

- Manhattan: We thrive in simplifying the property selling process even In the highly competitive Manhattan real estate market.

- Staten Island: If you need assistance in any part of Staten Island you can count on our team.

Real Stories: How We’ve Helped Homeowners

Here’s what a few of the many satisfied clients have to say:

Client 1: “Elite Properties made my home selling process very simple. The job relocation pressure drove me to move quickly which led to a swift cash transaction within seven days!”

Client 2: “I was overwhelmed by the thought of foreclosure until Elite Properties came to assist with a fair cash offer. The team protected my credit score as well as my mental peace.”

These stories highlight how Elite Properties transforms the home-selling experience for homeowners in need.

Conclusion: It’s Time To Sell Your Home with Confidence

At Elite Properties, we have redesigned the selling process to become fast, simple, and completely stress-free. Our trusted status as a professional house-buying company allows us to tailor solutions that let you walk forward in life.

Reach us at 718-557-9261 to start today or visit our website for your deserved cash offer. Elite Properties will manage your home sale process to provide you with a seamless transition to your next step in life.

Frequently Asked Questions (FAQs)

- When is the right time to sell my house?

Spring tends to be the preferred season due to heavy market interest though specific local conditions and lifestyle needs determine the optimal selling period.

- How do I figure out the best price for my home?

Home sellers can determine competitive pricing through local market research or by ordering a comparative market analysis CMA from licensed real estate experts.

- Do I need to repair my home before selling?

Selling your home as-is to a trusted buyer stands out as an excellent solution when time and resources run low even though property repairs have the potential to boost market value.

- What are the costs involved in selling a home?

The standard expenses, property sellers need to cover consist of agent commissions, closing expenses, property maintenance work, and house staging costs. Selling to Elite Properties saves property owners from having to pay numerous expenses.

- How long does it take to sell my house?

If you choose Elite Properties to sell your home it can happen in just several days instead of taking months like traditional sales.

A Security Deposit is a sum of money paid to guarantee the use of a piece of property. This phrase associates itself with leasing or renting an apartment. It can also refer to situations where a security deposit is necessary. The Security deposit for renting a home is an essential thing. You should take care of it before going out there to look for a rented place.

Security deposits, often known as “damage deposits,” are either refundable or nonrefundable. This means you may or may not be able to recover your money. It’s beneficial to know when and why a security deposit is a must before providing it.

Security Deposit Definition and Examples

A security deposit, in its broadest sense, is money you pay to someone else as part of a contract to utilize their property or services.

The landlord can keep your deposit if your lease contract permits it to pay any financial losses or damage they suffer as a result of your activities.

What are the basics of a Security Deposit?

How does A Security Deposit work?

The laws can dictate:

- How much can a landlord want as a security deposit?

- When are security deposits due?

- Where must this money be kept?

- When can I get my security deposit back, and how long do I have to get it back?

- When does a landlord have the right to hold a tenant’s security deposit?

Your landlord can keep all or part of your security deposit to cover cleaning and repairs. This happens if you vacate an apartment with stained carpets or broken fixtures. You can also look for FAQs when it comes to Security Deposit.

You may lose your deposit if you violate your lease and leave early. The deposit will be used to cover any remaining rent payments.

Landlord-tenant regulations may also outline what options you have as a renter for reclaiming your security deposit. If you suspect your landlord is unjustly withholding your deposit, you may be eligible to bring a civil complaint in small claims court.

Do You Need a Security Deposit?

When you rent an apartment or another place to reside, the landlord will almost always require a security deposit. If you don’t have the funds to pay a significant deposit upfront, you might be able to negotiate an alternate deal.

For example, you can split the deposit over the first three months of your lease term. Let’s get to know key takeaways about Security Deposit for Renting.

Key Takeaways

- The payments made in advance as a part of the contract to get access to the property is a Security Deposit.

- When renting a property, the lease agreement should specify the security deposit. The landlord-tenant legislation governs the lease agreement.

- Depending on the conditions of your agreement with a service provider or landlord, security deposits may be refundable or non-refundable.

-

If your security deposit is not given in an unfair manner, you can sue them in civil court to get it back.

Additionally, refer experts from Elite Properties who can assist you in making the right decision. We are a cash buying company that suggests we provide fast closings. Call us at 718-977-5462 today.

The necessity to relocate is one of the most common reasons for people to sell your home quickly. In areas such as Washington D.C., Maryland, Virginia, and Pennsylvania areas, there are numerous government and military employers and employees, which frequently necessitate migration. The need to buy real estate is increasing day by day.

Moving is necessary for other life transitions. Downsizing for retirement, relocating to a warmer climate to avoid our harsh winters, or a variety of other circumstances may necessitate the sale of a home.

We’d like to tell you about our approach if you need to relocate and sell your house fast in Maryland, Washington D.C., Virginia, or Pennsylvania for any reason.

Repairs are not needed to sell your home.

Even if your home is in good shape, there are always several issues that need to attend to before it is going to sell. The expenditures might build up, the time commitment can be lengthy, and repairs can be inconvenient. With Elite Properties you don’t have to be concerned about these fixes. We will buy your house as-is, whether it needs major renovations or minor ones.

There are no commissions or fees.

The majority of the time, sellers must pay commissions and fees to both their real estate agent and the buyer’s agent. So, if your house sells for $200,000, you’ll have to deduct around $12,000 from the amount and pay it to your real estate agents. There are no commissions or fees when you sell to Elite Properties.

Cash Offer that is both quick and reasonable

We realize the need for speed when relocating and your hectic schedule. When you cooperate with us, we’ll set up a same-day appointment to make you a reasonable cash offer. For you, it’s quick and simple! You can also choose your exact closing date when selling to Elite Properties Homebuyers, ensuring that the sale of your house fits into your schedule.

You can also choose your exact closing date when selling to us, ensuring that your property sale works into your schedule.

We Assist you with your relocation

In many cases, we can assist our clients in packing, organizing, decluttering, and relocating to their new homes. Another way we make the procedure as simple as possible for our valued clients is through this method.

What options do you have if you need to relocate for work?

Option#1: You can request a cash offer on your home.

Option#2: Hire a Real Estate Agent to sell your home.

- De-clutter and clean the house to make it appear bright and fresh.

- Improve the outside appearance

- Take care of any mechanical problems ASAP

- Set the appropriate price using the CMA.

Option#3: Rent your house instead of selling it

Bottom Line

At Elite Properties, we strive to make the process as simple and stress-free as possible for our clients.

You don’t have to bother about fixing your house, hiring an agent, paying commissions and fees, hosting open houses, or being subject to the schedules of possible buyers if you don’t want to.

When we say we buy properties for cash and as-is, we mean it. No repairs, no inspections, no open houses, no agent fees, and a quick closing are all options for selling your home.

Refer experts from Elite Properties who can assist you in making the right decision. We are a cash buying company that suggests we provide fast closings. Call us at 718-977-5462 today.

We’d love to meet you and be delighted to demonstrate how simple the sales process may be. Get started right away with a free quotation!

As far as residential real estate is considered, sellers of homes with certain problems or flaws may hear a piece of advice from their friends or family that they must simply “put a coat of paint on it” or “that’s the succeeding owner’s problem.” You also have to work with real estate disclosures.

What the majority of sellers fail to realize is that they are usually required to disclose specific information to prospective buyers. Real Estate disclosures are meant to inform potential buyers of any hitches with the property that might have an impact on its value or use. “Buyer beware” only holds as far as certain issues are considered.

Now, we are aware that selling a house can be exhausting, and we are here to make the process as stress-free as possible. This is why we wanted to ensure that homeowners recognize common disclosures that could have an impact on the sale of their homes. We’ve put together certain information that will update you on the realities as a seller.

Disclosure Basics

The necessities for real estate disclosures vary centered on state law. Some states lean severely towards buyer protection and command multiple pages of real estate disclosures, while other states adopt a buyer-beware approach.

What exactly is a seller’s disclosure form or seller disclosure statement?

Why Disclose?

Real estate disclosures are there to offer help to protect all parties involved in a sale. Homebuyers, of course, need to be aware of what exactly they’re getting themselves into with a specific property.

Sellers are secure by disclosures in two main ways. First of all, disclosures lessen the chance of buyers backing out at the last minute. Secondly, properly following disclosure law safeguards sellers lawfully. If a seller failed to disclose information that is must by state or federal law, the buyer can file a lawsuit years after the transaction in some areas. But, disclosures can bring some very grave issues to light and decrease the number of latent buyers who will want to deal with the disclosed issues.

Let’s get right to the most common ones now.

5 Common Real estate Disclosures

If you’re rolling up your sleeves to sell a property, you must be aware of these 5 common disclosures. Not all of them hold in every state, so ensure your own state’s rules.

-

Lead:

For the houses built before 1978, you’ve to disclose the existence of lead paints and their hazards. Sellers should also provide buyers with any records they have involving lead on the property, a lead warning statement, and a pamphlet created by the U.S. Environmental Protection Agency (EPA). This is the only federally instructed real estate -

Water Damage:

Water damage caused due to leaks and floods can result in health problems by creating mold and can compromise the structure of the house. This damage is not always apparent while the sale particularly if the sale is not taking place at the time of the rainy season. Many states necessitate sellers to disclose leaks and water damage. -

Legal Issues:

Maximum states also call for sellers to reveal any legal issues with the property. These issues could comprise the existence of property liens, building code desecrations, easements on the property, or boundary line disputes with the neighbors. The legal issues will have an impact on the potential new owners. So, it should be disclosed to the buyer. -

Structural And Mechanical Issues:

You must disclose any Mechanical and Structural Issues to the property. This would accommodate issues with the plumbing, electrical systems, heating, air conditioning, or structure of the home. Some states have a very precise form to fill out concerning the condition of each household system, while other states just need you to inform the potential buyer about any key problems. -

Neighborhood Annoyances:

Many states involve you to inform potential buyers about neighborhood nuisances.Neighborhood annoyances may include late-night parties, invasive odors, or violent dogs. Anything that would have an impact on buyers’ enjoyment of the home and neighborhood has to be revealed.

Consequences Of Disclosing

Disclosing properly is the way to go. But what will ensue after you disclose? Mostly, buyers will oversee smaller issues if they like the house, mainly in a hot market.

When it comes to greater issues, the buyer may ask you to fix something before the property changes hands, or they may ask you to take some money off the purchase price. If you and the buyer can’t agree, the buyer may walk away compelling you to begin the entire process all over again.

When In Doubt, Disclose

As we stated, required disclosures fluctuate by state. If you’re confused about disclosure, it is best to err on cautiousness and then disclose it. In addition to the liability benefits, disclosing meticulously helps buyers know that they can trust you as the seller sufficient to go through with the deal. And of course, it’s just the right thing to do! Referring to a real estate attorney can help ensure you’re doing everything appropriately.

Avoid The Trouble By Selling To Elite Properties

If you’d like not to worry about disclosures and how buyers will respond, there’s an easier solution.

At Elite Properties, we buy homes as-is and offer you a fair cash offer. We pride ourselves on providing a trouble-free selling process. This aids you in moving out quickly, without any of the hassles of fixing or selling your house. Call us at 718-977-5462 today.

Is It Time To Downsize Your Home?

Choosing the right time to downsizing the home or real estate property can be difficult. We’re often emotional when it comes to our homes or real property, and it can be tough to move on from a home that’s been associated with us. So how do you decide that it’s truly time to move on?

As real estate experts, we buy houses, and the team here at Elite Properties has assisted thousands of people to stand by this decision.

And here’s what we are aware of: If one of the five situations below applies to you, it could be the appropriate time to downsize.

Situation 1# Your finances have changed.

If your income has outdone your expenses, downsizing can aid you in getting back to a sustainable financial situation. You may have moved from two incomes to one, or your hours at work have been slashed. Maybe your taxes and utilities have escalated. When we buy houses, we often realize these are the reasons from our clients.

Whatsoever the reason for your current financial status, be aware that a smaller house usually costs less to maintain. And in case you’re already having concerns paying the mortgage, ensure you’re aware of all your options!

Situation 2# Your household has changed.

This can occur for many reasons—a few positive and a few negative. If your kids are college-goers, if you’ve undergone a divorce, if you’ve lost a near and dear family member—all these family changes will probably impact how much of your home you’re actively using. If your house has extra rooms and a three-car garage when you own a single car, it’s time to downsize.

Situation 3# You’re traveling quite a bit.

Are you among those lucky retirees who are spending most of their time traveling? Or does your job keep you in the get-set-go mode? Because we buy houses, we have worked with several clients that have government or military jobs that keep them away from home for longer periods. Downsizing might seem appropriate to you. When you save money on home costs—mortgage, taxes, utilities, and upkeep—you can put that extra money (and of course time!) towards your travel and other activities. Are you a snowbird who goes south for a good half a year or you’re planning several different trips overseas for work or pleasure, there’s no point in expending a lot on a home you hardly use?

Situation 4# You don’t want the maintenance.

If you’re having a worry about keeping up with the maintenance of a larger home, downsizing can be the right option for you. Or maybe it’s just that your main concerns have changed and you value having free time at hand over having a bigger house. You don’t wish to be mowing a big lawn or setting the right faucet leaks when you could be reading or relaxing!

Whatever the reason could be, decreased capability or desire to spend time on home maintenance can be a great motive to downsize. As simple as that, your home should be a source of enjoyment, not exhaustion or frustration.

Situation 5# You’d like to age in place.

If you decide to stay independent, it is logical to downsizing the home and get yourself set up to age in place. Maintenance is one of the key factors, but it goes beyond that.

To age in place, you’ll perhaps desire a single-level, accessible home. Whether or not you use any mobility aids at present, you’ll want to make sure everything is accessible to a wheelchair or walker. You may need wider doorways, gadgets that are operable from sitting height, and grab bars in basic locations. Without a doubt, these accommodations can be put in almost any house. But it’s quite easier and less costly to make a smaller home accessible. We specialize in buying houses that our clients want to move from and settle in a more accessible home.

Elite Properties Homebuyers

If you’ve opted to downsize, we’re ready to help.

We’ll offer you a quick and fair cash offer for your present home(real estate property) just as it is now; no repairs, no inspection, no commissions or fees. You can even decide on your exact closing date to coordinate faultlessly with the purchase of your new, smaller home. Our team will walk you through every step of your quote. This includes a review of what your home would likely bring on the open market.

Additionally, refer experts from Elite Properties who can assist you in making the right decision. We are a cash buying company that suggests we provide fast closings. Call us at 718-977-5462 today.

Transactions come in all shapes and sizes, but they usually involve two parties: the buyer and the seller. Once a buyer pays for an item or service, they can take ownership of it. However, purchasing property is a bit different in that there’s usually a lot of paperwork involved before you can claim ownership. One of the most important documents you’ll come across when buying property is the property deeds.

What are Property Deeds?

Property deeds are legal documents that establish the new ownership of real property. Real property is land or anything attached to it, like buildings or roads. A deed must identify the grantor and grantee, and provide a sufficient description of the property. It’s important to understand how property deeds work to ensure a smooth transition of ownership.

Deeds are legal documents and they are used to transfer ownership of property. In order for a deed to be legally binding, it must contain certain information, such as the names of the parties involved, a description of the property, and the date of the transfer. There are different types of deeds that can be used for different purposes, such as warranty deeds, quitclaim deeds, and special purpose deeds.

Livery of seisin was the old-school way of transferring real property. The person giving up the land would hand over a twig or clod of turf to the person receiving the land. A verbal or written statement would accompany the gesture, but it was the livery of seisin that made the transfer legal. Real property is conveyed by a paper deed.

Deeds are often seen as more official than other types of documentation. They are often a result of a court or legal ruling. However, they can also be private. They are executed by a deal between two or more individuals or businesses.

Necessary Information included in Deed

The content of a deed varies depending on the type of deed, but most deeds will include the following information:

- The property description, including its boundaries, adjacent roads, and utilities;

- The names and signatures of the seller and buyer;

- A clause authorizing the transfer of ownership of the property; and

- The final price of the property.

Critical Deed Elements

While each state has its necessities, the majority of deeds must contain several critical elements to be legally valid:

- They must be in writing.

The majority of deeds come in printed forms and have no legal constraint on them. All it should include are the essential elements of deeds.

- The grantor must possess the legal capacity to transfer the property and the grantee must be capable of receiving the grant of the property. If a person can draw a contract with legal force, that individual is considered to be competent to serve as a grantor.

- The grantor and grantee must be recognized in such a way as to be ascertainable.

- The property must be sufficiently described.

- Operative words of conveyance must exist. All standard form deeds contain the necessary legal language that essentially transfers the property.

- The deed must be signed by the grantor or grantors in case the property is owned by more than one individual.

- The deed must be legally conveyed to the grantee or someone acting on the grantee’s behalf.

- The grantee must recognize the deed. But he can refuse delivery of the deed in certain circumstances.

Types of Deeds

Deeds are of various categories. They may be official or private. Official Deeds and implemented under court to legal proceedings. Most property transactions, though, contain individuals and business entities using private deeds.

We can classify deeds according to the type of title warranties. The different types of deeds are as follows:

General Warranty Deed

The general warranty deed bids the grantee the utmost protection. With this type of deed, the grantor makes a series of legally binding promises (called covenants) and warranties to the grantee (and their heirs) agreeing to safeguard the grantee alongside any prior claims and demands of all persons whomsoever in regards to the conveyed land. The usual covenants for title involved in a general warranty deed are:

- It is the covenant of seisin, denoting that the grantor warrants they possess the property and has the legal right to transfer it

- This is as the covenant against encumbrances, signifying that the grantor warrants that the property is free of liens or encumbrances, excluding as specifically stated in the deed

- the covenant of quiet enjoyment. It signifies the grantee will have quiet possession of the property. And it will be true if the grantor has a defective title.

- There is a covenant of further assurance, where the grantor assures to deliver any document necessary to make the title good

Special Warranty Deed

Whereas in a general warranty deed, the grantor assures to warrant and defend the title carried out against the claims of all persons, the grantor of a special warranty deed warrants that they acknowledged the title to the property and that they have not done anything while holding the title to create a defect.

The defects that arose during the grantor’s ownership are in warranty. Because of this restraint, the special warranty provides the grantee less protection than the general warranty deed. Several purchasers of real estate will assert a general warranty deed to guard against problems that could arise as a consequence of a special warranty deed.

Quitclaim Deed

The quitclaim deed, also called a non-warranty deed, offers the grantee the least amount of protection. This type of deed conveys whatever interest the grantor currently has in the property—if any. There are no warranties or promises of the quality of the title. If the grantor has a good title, the quitclaim deed is essentially as effective as a general warranty deed.

However, if the title contains a defect, the grantee has no legal recourse against the grantor under the deed. A quitclaim deed comes into use when the grantor wants to avoid the liability under title covenants or is unsure of the status of the title.

Special Purpose Deeds

Special purpose deeds exist in connection with legal procedures and situations. It happens when the person acting on behalf of the government executes the deed. Utmost special purpose deeds offer little to no protection to the grantee. They are quitclaim deeds. Below are examples of special purpose deeds:

- Administrator’s Deed: This deed is viable when a person dies intestate. The court-appointed administrator reviews the decedent’s assets. This helps to transfer the ownership of the real estate to the grantee.

- Executor’s Deed: When a person dies estate, the executor’s deed comes to use. The estate’s executor will distribute the asset of the decedent. He will convey the title to the grantee.

- Sheriff’s Deed: A successful bidder at an execution sale receives a sheriff’s deed. It equates to the judgment that has been against the owner of the property. The grantee accepts whatever title the judgment debtor has.

- Tax Deed: When a property is in trade for delinquent taxes is a Tax Deed.

- Deed in lieu of Foreclosure: This is a legal document between the borrower and the lender who is in default on a mortgage. The lender agrees to allow the borrower to avoid foreclosure proceedings. This happens if the lender agrees to take the deed instead of foreclosure. Many lenders favor foreclosing to clean up the title.

- Deed of Gift (Gift Deed). Deed of gift transfers Real Estate title without contemplation or token consideration. It is mandatory to record the gift deed within two years in the near states.

What is Real Property?

Real property is not just a piece of land that you can touch and see, but the real property is also the materials that make up the land, such as buildings, trees, and any other structures. Real property is also known as real estate. It is a legal interest in land and anything permanently attached to the land. Real property can also include items that are above the ground, like antennas. In the US, real property is usually refer to as a real estate.

Real property works in a legal context. It is a property in which there is a real right to possession and use. You have to fill out forms for the transfer of Real Property.

The Bottom Line

However, refer experts from Elite Properties who can assist you in making the right decision.

We are a cash buying company that suggests we provide fast closings. Call us at 718-977-5462 today.

The Department of Veterans Affairs (VA) assures a share of a VA home loan when veterans use their remunerations to buy a home. A VA home loan lets veterans’ avail of home loans with more promising terms than a non-VA loan. You might be wondering how do VA home loans work. Let’s get right into it.

These loans have plenty of benefits, such as demanding no money down, no private mortgage insurance (PMI), and better rates than you might otherwise be able to get. In this blog, we will tell you about the benefits of a VA loan and how they work.

Definition and Example of a VA Loan

The U.S. Department of Veterans Affairs (VA) doesn’t finance money; loans are provided by private lenders. Still, VA promises a share of the loan that it will cover if you fail to pay, also called the entitlement. This may make lenders ready to offer more encouraging terms for veterans. Below video consists of how do VA loan work and what are its benefits.

The VA loan was formed in 1944 to remunerate veterans returning from World War II for their service, by making it easier for them to get into a home with a reasonable mortgage. It continues to be one of the most prevalent mortgage programs today. For instance, in 2021, over 1.4 million VA loans were granted for home purchases. There’s a motive behind the program’s fame, and it has to do with some VA home loan benefits.

How Do VA Home Loans Work?

VA home loans are a fabulous way to save money on a mortgage due to their unique cost-saving tricks. Here are the key VA loan benefits.

1. No Down Payment

For the majority of people, the major benefit of the VA loan is that you don’t need to put any money down. It’s one of the limited outstanding programs that still allows this. Since saving up for a down payment is often a blockade to homeownership for many people, this can be an enormous help.

VA Loan Savings at Closing

| Loan Amount | 0% down | 5% down | 10% down | 20% down |

| $150,000 | $0 | $7,500.00 | $15,000.00 | $30,000.00 |

| $250,000 | $0 | $12,500.00 | $25,000.00 | $50,000.00 |

| $350,000 | $0 | $17,500.00 | $35,000.00 | $70,000.00 |

| $450,000 | $0 | $22,500.00 | $45,000.00 | $90,000.00 |

2. No PMI

Usually, if you put less than 20% down with a conventional loan, you’ll have to pay for private mortgage insurance (PMI). This safeguards the lender if you default, and it can tack a heavy amount onto your monthly mortgage payment.

PMI Savings per Month

| Amount of Loan | Monthly Savings |

| $150,000 | Save $115/month |

| $250,000 | Save $191/month |

| $350,000 | Save $268/month |

| $450,000 | Save $345/month |

There’s no monthly PMI payment with VA loans, even if you put zero down. This excludes a huge cost and makes your monthly payments more reasonable right from the beginning

3. Flexible Credit Requirement

The VA doesn’t have the least possible credit requirement to get a VA loan. Still, individual lenders have credit necessities that you’ll need to meet to qualify for a VA loan.

VA loan requirements are usually easier to meet than those for an old-style mortgage. Most lenders need a credit score of 620 to qualify. That’s a lot less than the 753 average credit score for traditional mortgage holders in 2020. It’s also stress-free to buy another home sooner with a VA loan if you’ve run into credit hitches in the past, such as a foreclosure (even if it happened on a VA loan). You’ll only need to wait for two years prior to using your VA loan benefits again

4. Assumable

One exclusive benefit of a VA loan is that you can hand over the mortgage to the buyer when you sell your house. After they buy the home and the mortgage is transferred, you’ll be free from the loan, and the buyer will stay back to make the payments.

Having this ability to transfer, the mortgage can be a significant selling point if you locked in a low rate at the start of your loan and rates have gone up since then.

5. Limits on Closing Costs

If you avail of a VA loan, the seller will be required to pay definite closing costs, inclusive of the commission for the buyer’s and seller’s agent and a termite report. It’s voluntary for the seller to pay other fees, such as the VA funding fee for your loan or the appraisal fee.

If you can discuss having the seller pay these optional fees, you can’t ask them to pay more than 4% of the amount of loan

6. Lifetime Benefit

You can make use of your VA loan benefit over and over again for the rest of your life. So even if you’ve ducked on a VA loan in the past, or your Certificate of Eligibility (COE) says “$0 basic entitlement,” you may still be able to get a VA loan. Additionally, there are no limits to the amount of loan you can get.

You may also be able to have two VA loans at a single shot or get a jumbo VA loan if you’re buying a home above the FHFA (Federal Housing Finance Agency) conforming loan limits in your area—$647,200 for most areas and up to $970,800 in high-cost areas.[1]

7. Lower Rates

VA loans have a greater up-front cost with the VA funding fee, which is calculated as a percentage of the whole amount of your loan. The funding fee aids in reducing the cost of VA loans to taxpayers.

VA loan rates are usually lower on average. For instance, in September 2021, VA loan rates averaged 0.32% lower. That may not seem like a huge difference, but it could save you tens of thousands of dollars throughout the life of the mortgage.

FAQs about how do VA loans work.

What do you require to prove you’re eligible for a VA loan?

- If you’re a veteran, you’ll need a copy of your DD-214 and be entitled to receive VA benefits.

- If you’re an active-duty service member, you’ll require a statement of service describing your personal information and service details.

What are the service necessities for a VA loan?

- The service requirements fluctuate depending on when you served, when you separated from service and part from the fact whether you were discharged with a service-connected disability.

- Active-duty service members and veterans have service necessities that differ between 90 days and 24 continuous months.

- National Guard and Reserve members have a minimum of 90 days of active-duty service.

Additionally, refer experts from Elite Properties who can assist you in making the right decision. We are a cash buying company that suggests we provide fast closings. Call us at 718-977-5462 today.

For more information on how do VA home loan work as well as Mortgage Home Loans feel free to visit.

1. Sales need 12 to 18 Months For Closure:

The fastest you will be able to close any short sales listings is at least 14 days. Even when a cooperative bank holds your loan. The lender needs seven to ten days to grant a receipt for the short sale package. It also includes personal seller documents and related real estate items.

Here, we present the time frame for an average short sale. Especially when the loan is held by a cooperative bank. Seven to ten days for the lender to grant receipt of the complete short sale package, which entails personal seller documents and related real estate items, together with the buyer’s short-sale offer.

a. A negotiator is assigned. The BPO or appraisal needs around 30 days to 45 days.

b. Extra two to three weeks for management/review by investor and short sale approval. Every short sale is exclusive, and every set of investors is diverse. The examining bank might not own the loan, so they must follow investor guidelines. You cannot blame some short sale bank as there were unreasonable to you or you hate them for a specific time.

2. Short Sales Buyers Pay Quite Huge Amounts:

3. Short Sale Banks Won’t Agree to An Extremely Discounted Payoff:

Sellers seem amazed by the fact that prices have dropped over five years resulting in 50% or less than the OG value. Banks know declining markets.

Moreover, banks will carry out their research about the value and sum up a conclusion. The home value is just not based on the amount of the mortgage. It’s based on the present comparable sales too.

4. Short Sale Sellers Must Be In Default before the Bank Approving A Short Sale:

Banks favor a short sale grounded on the seller’s hardship and the value of the home. Some sellers work hard to make the mortgage payments each month, yet they are not faulted.

While it is a fact that, true that sellers in default receive instant attention, a seller can also pay a mortgage payment on time every month and still be suitable for a short sale. The seller can buy another house under Fannie Mae’s criteria if they are regular on their loan.

5. Agents Get A Lower Commission:

In the early days, the short sale commissions were not handled well by the banks, between the years 2005 to 2008.

The majority of banks now pay an old-fashioned commission to agents. On February 24, 2009, the Federal National Mortgage Association created a compensation policy. The policy allows paying of the agreed commission by the seller to the listing agent. This commission did not exceed 6%. The borrowers can qualify for Home Affordable Modification Program(HAMP) by the government. They can also apply for Home Affordable Foreclosure Alternatives (HAFA) program.

Additionally, refer experts from Elite Properties who can assist you in making the right decision. We are a cash-buying company that suggests we provide fast closings. Call us at 718-977-5462 today.

Adverse possession is a legal guideline when someone obtains the title of another person’s property or land. Elements of Adverse Possession and their Rules differ by jurisdiction. But usually, somebody can claim adverse possession after they’ve taken up residence on or have uninterrupted ownership of a piece of property for a definite amount of time.

In this blog, we help you learn more about what is adverse possession, the legal norms for that classification, and how it could affect you as a property owner.

What is adverse possession in real estate?

Adverse possession endows possession of land to someone apart from the owner if that person inhabits it for longer than the order of limits for that jurisdiction. Adverse Possession is a strange law where someone occupies property without permission. Also, then acquires a legal right to that property once a set amount of time has passed.

What are the 5 requirements for Adverse Possession?

The requirements for asserting an adverse possession claim vary from state to state, but there are two main reasons why these requirements exist.

- The first reason is to give the rightful owner of the property a chance to stop the adverse possessor from taking over through several different methods.

- The second justification is that adverse possession allows for the property to be put to good use instead of sitting unoccupied and undeveloped.

Understanding the requirements is crucial for individuals seeking to claim ownership of property through statutory ownership. To address the query, “What are the 5 requirements for adverse possession”, a legal concept in real estate, entails five essential conditions:

- Open and Public: Adverse possessors must be using the property openly and notoriously. This means that the user cannot be hidden from view. This would allow the true owner to see the use and stop it. If the adverse possessor’s use is happening in secret, the owner may not learn of it until it’s too late to assert their own rights.

- Hostility Claim: The claim of someone who uses adverse possession must be against the owner’s use of the land. This means that the adverse possessor may not make an adverse possession claim if the owner permitted them to use the land.

- Continuous Possession: To qualify for adverse possession in New York, the trespasser must have had exclusive and continuous possession of the land for at least ten years. This means that they cannot have left the land for any significant periods during those ten years.

- Actual Possession: The individual must physically occupy the property and use it as a true owner would. Mere intentions or occasional use are usually insufficient; there must be tangible occupation.

- Exclusive Possession: The possession must be exclusive to the adverse possessor and not shared with the true owner or others who also claim ownership rights. Joint use with the owner typically doesn’t qualify.

Also, one additional requirement is Time Period. All states have a time limit in which the adverse possessor must use the land before it officially becomes theirs. In New York, the law requires that land must be used for a minimum of ten years before the adverse possessor gains title to the property.

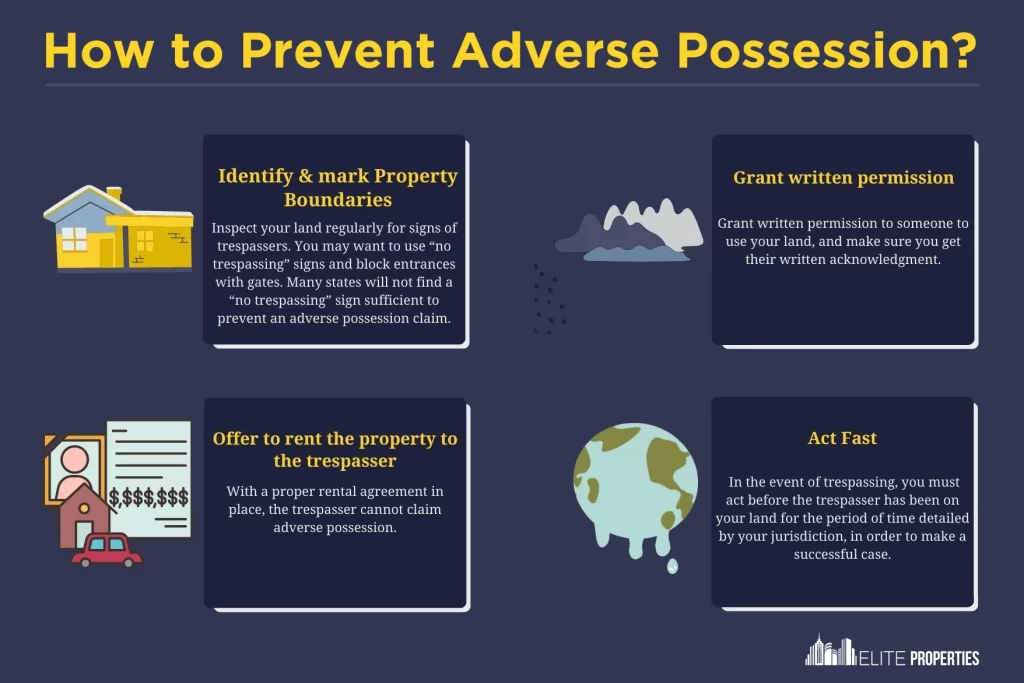

How to Prevent Adverse Possession?

- Regular Property Checks: Conduct regular inspections of your property to identify any unauthorized use or occupation. Attention is key to catching potential adverse possessors early on.

- Maintain Clear Boundaries: Mark your property boundaries with fences, walls, or signs. This helps to establish the limits of your property and discourages encroachment by others.

- Document Property Use: Keep detailed records of your property use, including maintenance activities, improvements, and any notices sent to potential encroachers. This documentation can serve as evidence of your active ownership.

- Communication with Neighbors: Encourage open dialogue with neighboring landowners to resolve boundary concerns promptly, preventing potential misunderstandings that could result in occupancy claims.

- Regular Property Use: Not only consistently utilize but also maintain your property according to ownership rights. Active involvement with your land strengthens your ownership claim also minimizes the chance of others claiming encroachment.

- Legal Action When Necessary: If you discover unauthorized use of your property, swiftly pursue legal steps to resolve it. This could mean issuing warnings, bargaining boundary agreements, or taking legal action such as eviction or trespassing charges.

- Monitor Legal Deadlines: Stay informed not only about the legal timeframe for prescriptive rights in your area but also the act ahead of time to avoid it. Consistently monitor your property and promptly address any potential claims to safeguard your ownership rights.

In What Way Does It Work?

Adverse possession is when a non-owner/trespasser/squatter inhabits real property deprived of consent. The owner must attempt to do away with them during the ruling of limitations period; otherwise, the person obligating the possession could possibly take legal ownership. However, for there to be adverse possession, each of the following criteria must be met

- Exclusive and continuous: The possessor has to have persisted on the property uninterruptedly, without others inhabiting it as well.

- Actual possession: The person must tangibly inhabit the property, not just mention that they want to control it.

- Hostile possession: The possessor, by inhabiting the property, is trespassing on the original owner’s rights without consent.

- Open and notorious possession: The possessor is not nagging onto the property. Not only they are amenably living there in a way an owner would, but also their occupation should be evident to any outside observer.

How to File for Adverse Possession

It’s crucial to understand the laws as well as procedures governing squatter’s rights in the relevant area and possibly seek legal advice to ensure compliance and increase the chances of a successful claim. Here’s what you should know about how to file for adverse possession:

- Consult with a real estate attorney: An attorney can assess your situation, determine if you meet the requirements for statutory occupancy in your specific jurisdiction, and guide you through the filing process.

- Gather evidence: You will also need documentation to prove you meet the five requirements for a claim of right. This might include things like property tax bills addressed to you, receipts for repairs or improvements made to the property, and affidavits from witnesses who can verify your exclusive and continuous use of the land.

- File a lawsuit: With your attorney’s help, you’ll need to file a case against the legal owner of the property. This case will initiate the legal process of claiming ownership through prescriptive rights.

Examples of Adverse Possession

Adverse possession can take place in a couple of ways.

- First, adverse possession could be granted to someone who purposely occupies property that doesn’t belong to them. Such as a trespasser or a squatter, who lives there for a long period of time. This may take place in the case of an absentee owner not checking on the property. If enough time passes per the state’s law, the title is transferred to the trespasser.

- The sum of time necessary to inhabit a property before initiating the its process differs by state and local law, usually taking more than a few years.

- Somebody could meet the requirements for adverse possession in as little as two years in Maricopa County, Arizona. Even though it’s more likely to see longer periods, for instance, 10 years in New York.

- In another mundane example of it, somebody such as a neighbor intrudes on a rightful owner’s property. For example, a neighbor may construct a garage or build a fence that crosses a property line. This at times is done unintentionally, but it could result in adverse possession. It’ll happen if the infringement occurred for long enough.

You can also go through the Laws of Adverse Possession of New York, to know more.

What Is the Time Limit on Adverse Possession?

The time limit for adverse possession, also known as the statutory period. It is the critical duration someone must occupy another’s property to claim ownership through squatter’s right. Also, it’s a key factor and varies depending on your location. Here’s a breakdown:

- No Single Time Limit: There’s no one-size-fits-all time limit across different countries or even states within a country.

- Range: The statutory period typically ranges from 3 years to 30 years.

Who Can Claim it?

In general, anyone who meets the legal requirements for encroachment can claim ownership of another’s property after a specific period. However, there are some limitations and exceptions to consider:

- Individuals: Any individual can potentially claim possessory title if they meet the requirements.

- Government Entities: In some cases, government entities like municipalities or states might be able to claim statutory ownership, but the rules may differ.

- Successors and Heirs: The rights to an adverse occupancy claim can sometimes pass to successors or heirs of the original possessor if they continue meeting the requirements.

Difference between Adverse Possession and Homesteading

| Aspect | Adverse Possession | Homesteading |

| Legal Basis | Based on occupancy without the owner’s permission | Based on government grants or laws |

| Intent | Does not require permission or intent to own | Requires intention to establish ownership |

| Ownership Transfer | Acquired by continuous use without owner’s consent | Acquired through government grant or specific laws |

| Duration | The statutory period of occupation varies by jurisdiction | Typically involves a fixed period of residency |

| Purpose | Often occurs unintentionally or through negligence | Intentionally seeks to establish ownership and settle |

| Requirements | Continuous, hostile, open, exclusive, and notorious possession | Compliance with government regulations and residency |

| Examples | Squatting on unused land without permission | Settling on public land under homesteading laws |

Bottom Line

Adverse possession can result in a legal headache for a property owner, but there are means to escape it. The best constraint for illegal inhabitants is to keep consistent tabs on a property. Ensure that there is a lock on everything and is fence-proof.

If the owner grants written permission to trespass on their property, then it would not be adverse possession. Still, be careful that permitting a neighbor to build on and/or encroaching on your land. They could cause problems if and when you try to sell.

Should you find yourself in a situation in which someone is on the verge of qualifying for adverse possession, hire an attorney to assist you in filing a lawsuit to remove the party and/or reclaim the property. Additionally, refer experts from Elite Properties who can assist you in making the right decision. We are a cash buying company that suggests we provide fast closings. Call us at 718-557-9261 today.

FAQ

1. How many years is adverse possession in NY?

Adverse possession in New York requires a continuous occupation of at least ten years to establish a claim to ownership of property. This duration is subject to specific legal requirements outlined by New York state law.

2. Can adverse possession be challenged?

Yes, it can be challenged through legal means. Such as filing a lawsuit to dispute the adverse possessor’s claim to the property. Challenges may involve proving that the holder neither meet all the necessary legal requirements nor demonstrating continued ownership and control of the property by the original owner.

3. What are the 5 main elements to obtain an adverse possession of a property?

The five main elements to obtain adverse possession of a property include continuous and uninterrupted possession, open and notorious use, hostile or adverse occupancy without permission, exclusive possession, as well as the statutory period of occupation, which varies by jurisdiction.

4. Does adverse possession apply to new owners?

Adverse possession laws can apply to new owners if the conditions are met. Regardless of whether they acquired the property through purchase or inheritance. However, new owners may have legal recourse to challenge claims if they can demonstrate continued ownership and control of the property.

5. What are two options to avoid adverse possession?

To avoid adverse possession, property owners not only regularly monitor their land but also address any unauthorized occupation promptly. Additionally, maintaining clear boundaries and actively using the property. Also, this can help prevent hostile possession claims from arising.

6. What is the shortest time for it?

The shortest time for it varies by jurisdiction but typically ranges from a few years to several years. However, not only specific legal requirements but also the conditions must still be met within this timeframe for encroachment to be established.